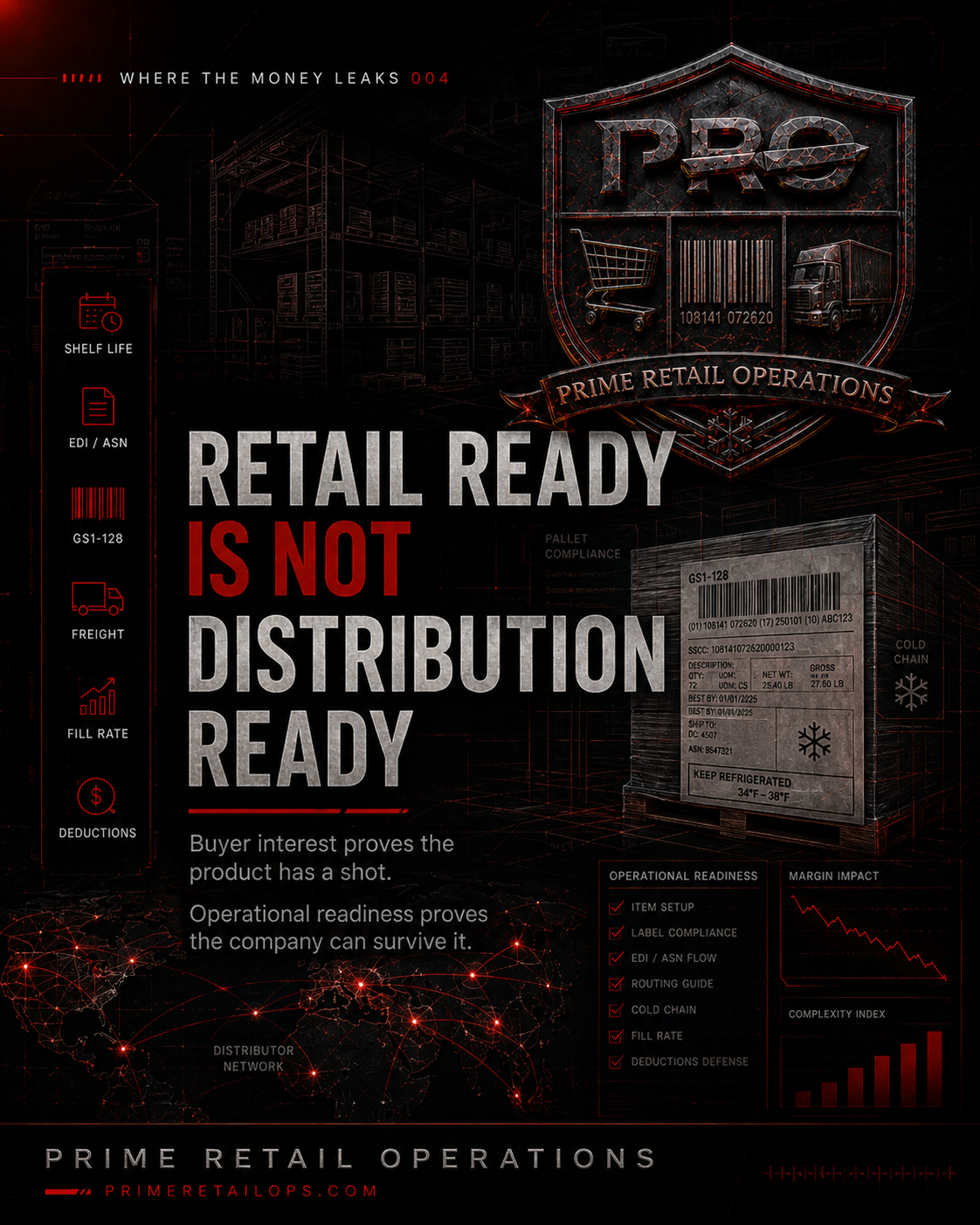

Retail ready is not distribution ready.

That is one of the most expensive lessons emerging CPG brands learn after the buyer says yes.

A brand can have a great product. Strong packaging. A clean ingredient deck. A compelling founder story. Good consumer feedback. A sharp sell sheet. Maybe even buyer interest from a respected retailer.

That means the brand has a shot.

It does not mean the brand is ready for distribution.

Retail readiness is front-end readiness. It proves the brand can earn attention. Distribution readiness is back-end readiness. It proves the company can execute after the attention turns into purchase orders, freight windows, code-date requirements, deductions, fill-rate expectations, promotional commitments, and working-capital pressure.

Those are very different tests.

A retail-ready brand can win the meeting.

A distribution-ready brand can survive the launch.

That distinction matters most in fresh, refrigerated, frozen, natural, organic, and specialty categories because the system is less forgiving. Shelf life matters. Temperature control matters. LTL freight matters. Case configuration matters. GS1-128 labels matter. ASNs matter. Fill rates matter. Deductions matter. Cash timing matters.

The product may be beautiful.

The warehouse does not care.

That is not a criticism of the distributor. It is the reality of the system. Regional, specialty, and broadline distributors are infrastructure. They create access to retail networks most emerging brands could never serve efficiently on their own. They are not brand incubators. They are not your sales agency. They are not your operations department.

They move product through a system that requires discipline.

If the brand creates friction, the system charges for it.

That friction can show up everywhere.

An ASN does not match the physical pallet. A GS1-128 label scans incorrectly. Product arrives short-coded. The fill rate drops. A shipment misses the appointment window. A promotion is funded without understanding the true deduction stack. A new DC opens before the brand has proven downstream pull-through. A broker secures the authorization, but the brand has no internal operating system to manage what comes next.

None of that looks dramatic on launch day.

It shows up later in remittances, deductions, missed reorders, aging inventory, spoilage claims, freight bills, and cash getting tighter while sales reports still look encouraging.

That is where the money leaks.

The biggest blind spot is assuming buyer interest equals channel readiness.

It does not.

A buyer can like the product and still be staring at a supplier that cannot yet support the channel. The first authorization is not proof of operational fitness. The first purchase order is not proof of consumer demand. Pipeline fill is not velocity. A DC setup is not a sales strategy.

The second reorder is where the truth starts.

So what does distribution readiness actually require?

It starts with margin architecture.

A brand needs to know true net landed margin before launch. Not theoretical gross margin. Not COGS plus markup. True net landed margin after freight, distributor programs, trade spend, deductions, spoilage, admin fees, promotional commitments, and working-capital timing.

If that number does not work, scale will not fix it.

It will expose it.

Then comes operational compliance.

The brand has to understand EDI, ASNs, case labeling, pallet labeling, appointment windows, routing guides, fill-rate expectations, and receiving requirements. These are not boring back-office details. They are margin-protection systems.

In refrigerated and frozen distribution, the margin for error gets even tighter.

If the product arrives late, warm, damaged, mislabeled, or short-coded, the brand owns the consequence. Cold chain does not forgive almost-ready operations. Every extra day in transit burns shelf life. Every small LTL shipment adds freight exposure. Every overbuilt pipeline creates inventory aging risk.

The broker can help open the door.

The brand still has to operate the room.

That is another blind spot. Brokers are valuable. Good brokers understand buyers, category timing, retail relationships, promotional windows, and how to position a brand. But a broker does not replace internal operating discipline.

A broker should not be the brand's demand planner, deduction analyst, freight strategist, EDI owner, working-capital modeler, and inventory controller.

That has to live inside the business.

Regional distribution can be a smart proving ground.

For many brands, the right answer is not to sprint straight into national broadline expansion. It is to prove velocity regionally, tighten the operating model, understand true economics, validate packaging and shelf life, build reorder discipline, and learn how the brand behaves inside a real retail environment before multiplying the number of DCs and retailers.

Distribution readiness is not about being afraid of scale.

It is about earning scale.

Sophisticated brands do not chase every door. They stage expansion. They protect working capital. They know which SKUs deserve wider distribution and which should stay regional. They understand when a promotion builds demand and when it only rents velocity. They monitor deductions. They track code life. They know whether the distributor is shipping out what they are shipping in.

They treat distribution as an operating system, not a trophy.

Operator Takeaway

Retail readiness gets the brand considered.

Distribution readiness keeps the brand alive.

Buyer interest proves the product has a shot.

Operational readiness proves the company can survive it.